The ever-changing shopping world always surprises with innovations, not only in emerging products, but also in the ways of purchasing them. Today, we will talk about one such innovation called Buy Now Pay Later, or BNPL for short.

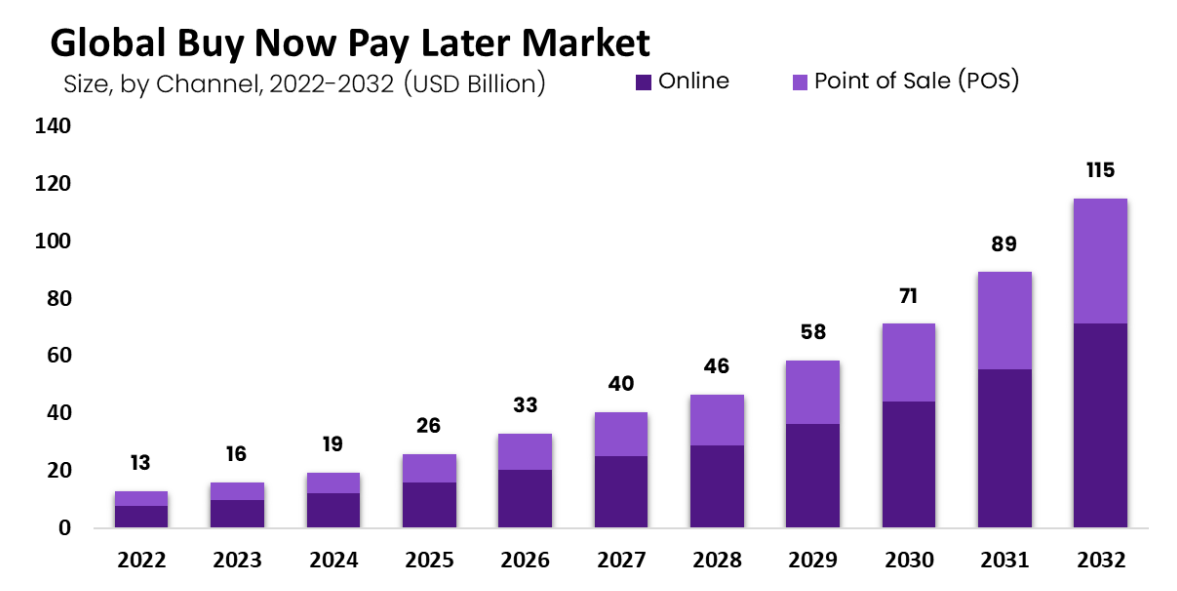

Just to put things in perspective, BNPL has evolved into a global industry, and according to the latest research, the global BNPL market size is about to hit $115 billion by 2034. It has expanded so extensively that it has shifted from the familiar B2C landscape to B2B — and e-commerce experts must stay abreast of these trends to avoid missing out on lucrative business opportunities.

What is Buy Now Pay Later (BNPL)?

If we describe BNPL simply, we can say it’s a modern version of layaway. With BNPL, you can get things you want immediately but pay for them later instead of right when you buy them. It’s super easy—just a click or tap, and you can take home your items without paying upfront. But while it might sound simple, a lot is happening behind the scenes that affects shoppers and businesses.

How does BNPL work for B2B?

Buy Now Pay Later (BNPL) is becoming popular for companies to handle their finances. Unlike the BNPL used by regular shoppers, B2B Buy Now Pay Later is a sort of arrangement by businesses that are buying from other companies.

Global BNPL Market Size Growth by Market.us, 2023

Basically, B2B BNPL is like a line of credit for businesses. It lets them buy what they need from suppliers without paying right away. Buy Now Pay Later is helpful for companies that need to manage their business supplies, cash flow or want to use their money for other things. With B2B BNPL, they can delay paying until a later date, often when they’ve made money from their own sales or hit certain milestones.

BNPL B2B deals are usually customized to fit the needs of each business and its relationship with suppliers. They might include things like setting credit limits, flexible payment schedules, or even discounts for buying in bulk or paying early. These personalized deals help strengthen the relationship between buyers and sellers.

B2B BNPL platforms can also make the buying process smoother. They integrate with existing systems, making it easier for businesses to place orders, get invoices, and reconcile payments. This saves time and reduces the chance of mistakes.

BNPL vs Traditional Financing

Breaking down the differences between Buy Now Pay Later (BNPL) and traditional financing sheds light on the contrasting landscapes of consumer finance.

| BNPL | Traditional Financing |

|---|---|

| Represents instant gratification and flexibility, allowing consumers to acquire goods without immediate payment | Follows conventional structures with credit checks and interest charges |

| Offers simple repayment terms and minimal credit checks | May incur interest and have stricter qualification criteria |

| Allows consumers to manage payments in smaller installments and avoid debt accumulation | May involve complex processes and eligibility criteria |

BNPL vs Credit Card

BNPL is all about getting what you want right away without paying upfront. You can split the cost into smaller payments over time, usually without any extra fees. This helps you manage your money better and avoid getting into debt. However, you might have to pay late fees if you miss a payment.

On the other hand, credit cards give you a line of credit with a spending limit. They come with perks like credit card processing, rewards and purchase protection, and using them can help you build your credit history. They’re widely accepted and offer more features than BNPL.

BNPL B2B vs BNPL B2C

Statistics from 2022 show that over 50% of the largest B2B platforms have already adopted the “Buy Now, Pay Later” principle. Over the past 2 years, this number has only grown, so it’s time to understand what this entails, isn’t it? Let’s compare how BNPL functions in B2B and B2C.

The Rise of Buy-Now-Pay-Later (BNPL) Services by Yodlee, 2022

If we examine Buy Now Pay Later (BNPL) in business and consumer contexts, we see some key differences that reflect each goal and need.

For consumers (B2C), BNPL is all about making buying easier and more flexible. It lets people immediately get things they want and pay for them later. This setup has features like flexible payment schedules and easy online experiences to suit individual shoppers who wish convenience and flexibility with their budget.

Read more: Buy Now, Pay Later: Benefits For ECommerce Sites

On the other hand, in business (B2B), BNPL is about making operations run smoother and managing money better. It helps companies get what they need from suppliers without paying right away. By letting them delay payments until later, B2B BNPL helps with cash flow and simplifies the buying process. It also helps build stronger relationships with suppliers.

B2B platforms often have special features tailored to meet the specific needs of businesses and their partners. These could include setting custom credit limits, handling invoicing and payments, and offering discounts for bulk orders or financing options.

Another big difference is in the risks involved. B2B transactions usually involve bigger amounts of money and longer payment terms, so there’s more focus on managing credit risks and following regulations to ensure payments happen smoothly and securely.

Want to boost your business with BNPL solutions?

Benefits of B2B BNPL

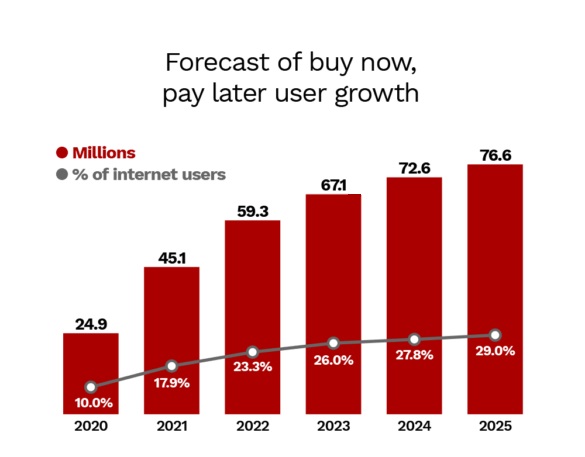

BNPL User Growth by eMarketer, 2021

While the B2C sector embraced the system long ago, why is it that the B2B sector is only now adopting it? The primary reason can be traced back to the series of crises in the 20th century. It became evident that no business could be considered completely immune to economic fluctuations, and obtaining trade credits for small enterprises was nearly impossible.

Nowadays, the adoption of Buy Now Pay Later (BNPL) solutions in Business-to-Business (B2B) transactions heralds myriad benefits for buyers and businesses navigating the intricacies of modern commerce.

Benefits of B2B BNPL for buyers

Using Buy Now Pay Later (BNPL) in B2B transactions has many advantages for buyers who are making company purchases:

- Enhanced Cash Flow Management. B2B BNPL allows buyers to maintain better control over their cash flow by deferring payment until a later date, aligning with their business cycles or project milestones.

- Optimized Resource Allocation. By postponing B2B payments, buyers can allocate financial resources more strategically, preserving capital for other operational needs or growth initiatives.

- Simplified Budgeting. BNPL’s transparent pricing structures and clear repayment terms make it easier for buyers to budget effectively and plan their expenses.

- Access to Value-Added Services. BNPL platforms may offer additional services such as integrated invoicing and reconciliation tools, risk management solutions, and tailored financing options to meet buyers’ specific needs.

- Increased Peace of Mind. Splitting payments into manageable installments over time helps buyers navigate budget constraints and unforeseen expenses, providing greater flexibility and reducing financial stress.

Benefits of B2B BNPL for merchants

Introducing BNPL options has many benefits that can help your company become more efficient, flexible, and competitive. Here’s how:

- Encourages More Spending. With BNPL, customers can buy more stuff, even if they don’t have all the money upfront. For example, if a customer is low on money during slow seasons, they can still make purchases and pay later when they have more cash. Offering BNPL can lead to bigger orders, sometimes even doubling the amount customers spend. BNPL for business is a perfect choice because it brings in more money and increases the average order of customers.

- Better Cash Management. B2B BNPL lets you buy what you need from suppliers without immediately paying for it. This means you can use your money smarter and keep it for significant investments or urgent needs.

- Reduced Financial Risk. Offering trade credit or invoicing after service can be risky because customers might pay late or not at all. With BNPL, you’re not dealing with payment plans or chasing down money. The BNPL partner takes on the risk, and you get paid immediately.

- Makes Financing Easier for Customers. Another benefit of Buy Now Pay Later for merchants is that it is more affordable and convenient than credit cards or loans. It often has lower interest rates than credit cards, and the approval process is quick. Customers can apply for BNPL right when they’re making a purchase without any hassle.

- Access to Helpful Services. BNPL platforms often offer extra tools and financing options tailored to your needs. This can include things like easier invoicing, better risk management, and flexible payment plans.

- Keeps Your Business Competitive. If your competitors offer BNPL and you don’t, you might lose customers. Nowadays, people expect BNPL as a payment option. Adding BNPL shows that you care about customer preferences and helps improve their shopping experience.

Learn more about BNPL benefits here: Buy Now, Pay Later: Benefits For ECommerce Sites

Risks in B2B Buy Now Pay Later

Utilizing Buy Now Pay Later (BNPL) can offer significant advantages for businesses engaging in B2B transactions, but it’s essential to remain vigilant against potential pitfalls:

- Cash Flow Management. Opting for BNPL entails delaying payments, necessitating careful cash flow management to ensure readiness for eventual payments. Inadequate cash flow management could lead to challenges such as overdue bills or even insolvency.

- Over Reliance on BNPL. While BNPL can provide temporary relief, businesses must evaluate whether they’re overly dependent. Excessive reliance on BNPL may indicate inadequate financial planning or poor long-term management, potentially leading to future complications.

- Additional Fees and Penalties. Some BNPL arrangements may include extra fees or penalties for late payments or non-compliance. Failure to adhere to terms and conditions could increase costs or strained supplier relationships.

- Impact on Supplier Relations. While BNPL can strengthen supplier relations by ensuring timely payments, it may also grant suppliers greater bargaining power. Businesses relying heavily on BNPL may encounter challenges negotiating favorable terms or securing competitive deals.

- Regulatory Compliance. Industries involving BNPL transactions are subject to stringent regulatory requirements. Non-compliance could result in regulatory penalties or damage the business’s reputation, emphasizing the importance of adhering to regulatory guidelines.

Best B2B BNPL providers

When it comes to choosing the ideal BNPL provider for your business-to-business (B2B) transactions, there are several crucial factors to consider. Reliability, flexibility, and alignment with your specific needs and preferences are paramount. Within the B2B space, numerous BNPL providers have risen to prominence, each offering tailored solutions to meet the distinct demands of corporate procurement. Here are some standout options:

Klarna

Recognized for its adaptability and intuitive payment solutions designed specifically for B2B transactions. Klarna offers customizable credit limits, transparent pricing, and seamless integration with existing procurement systems, empowering businesses to streamline their purchasing processes while nurturing robust supplier relationships.

Features:

- Customizable credit limits

- Transparent pricing

- Seamless integration with procurement systems

- Strong supplier relationship management

PayPal Pay in 4

Besides being one of the most popular payment methods worldwide, PayPal also provides businesses with a convenient BNPL solution for managing B2B transactions. With no credit checks, instant approval, and transparent repayment terms, PayPal Pay in 4 facilitates access to essential goods and services from suppliers while preserving cash flow flexibility.

Features:

- No credit checks

- Instant approval

- Transparent repayment terms

- Access to PayPal’s extensive network

Afterpay

Known for its simplicity, transparency, and adaptability in B2B transactions, Afterpay simplifies processes with straightforward terms, instant approval, and integrated invoicing capabilities. This fosters smoother transaction processes and strengthens supplier relationships, enhancing efficiency within the supply chain ecosystem.

Features:

- Simple terms

- Instant approval

- Integrated invoicing capabilities

- Strong focus on supplier relationship management

Affirm

Offering businesses a seamless and user-friendly payment solution tailored to their unique needs, Affirm provides flexible repayment options, transparent pricing, and integration with popular e-commerce platforms. This enables informed purchasing decisions while mitigating financial risk and optimizing cash flow management.

Features:

- Flexible repayment options

- Transparent pricing

- Integration with popular e-commerce platforms

- Focus on financial risk mitigation

Zip

Renowned for its innovative B2B BNPL solutions, Zip caters to diverse business needs with a range of payment options, including interest-free installments and credit lines. Its seamless integration with procurement systems and user-friendly interface make it an attractive choice for businesses seeking to streamline their purchasing processes.

Features:

- Range of payment options

- Seamless integration with procurement systems

- User-friendly interface

- Focus on diverse business needs

How to implement BNPL in B2B eCommerce

Implementing Buy Now Pay Later (BNPL) solutions in Business-to-Business (B2B) eCommerce requires careful planning to make sure it benefits both buyers and sellers. Here’s how to do it:

Step 1: Select BNPL Provider

Start with a thorough research of various BNPL providers to find the ones that best align with your business needs and goals. Consider factors such as payment processing capabilities, integration options, scalability, and reputation. Narrow down your choices to a select few providers that offer the features and services you require.

Some BNPL providers may offer limited integration options or lack support for popular eCommerce platforms, making it difficult to integrate their services into your existing systems. Inadequate technical support from BNPL providers can hinder the integration process and delay the deployment of BNPL functionality.

Step 2: Assess Your Infrastructure

Check your eCommerce setup and find BNPL providers that work well with your systems. Consider payment processing and how easily BNPL can be integrated into your setup.

Note that your current eCommerce infrastructure may not be compatible with certain BNPL providers’ systems or APIs, leading to integration challenges. Also, some legacy ERP systems or outdated payment processing software may lack the necessary features or APIs required for seamless BNPL integration.

Read more:

Outdated websites: When do you need a website redesign or website relaunch?

Step 3: Plan the Integration

When you have found a suitable provider, it’s time to start integration. First, develop a comprehensive integration plan that outlines the steps involved in integrating BNPL functionality into your B2B eCommerce platform. Determine the specific features and functionalities you want to offer through BNPL, such as flexible payment terms or installment options.

Remember that integrating BNPL functionality into your eCommerce platform may be more complex than anticipated, requiring extensive customization and development work. Ensuring the security of customer data and payment information during the integration process is critical and may require additional security measures to be implemented.

Step 4: Integrate BNPL

Collaborate with your chosen BNPL provider to implement the necessary technical integrations, such as secure payment gateways, APIs, and plugins. Ensure your BNPL provider’s options are seamlessly integrated into your checkout process. This makes it easier for buyers to use BNPL to complete their purchases.

At this stage, technical errors or bugs may occur during the integration process, leading to failed transactions, payment processing errors, or data synchronization problems. Optimizing the performance of BNPL integrations to ensure fast and reliable transaction processing may require fine-tuning and optimizing code and infrastructure.

Step 5: Set Clear Policies

Establish clear rules for using BNPL, like credit limits and repayment terms. This helps avoid problems like late payments and builds trust between buyers and sellers.

Step 6: Train Your Staff

After the BNPL solution is set, it’s time to teach your employees how to work with it. Provide training and educational resources to your internal team members to familiarize them with the BNPL integration and its features. Don’t forget to offer support and guidance to customers with questions or concerns about using BNPL for their purchases.

Step 7: Testing and QA

Changes made during the BNPL integration process may introduce new bugs or regressions into existing code, requiring thorough regression testing to identify and resolve issues.

Conducting thorough testing of the BNPL integration to identify and resolve any technical issues or bugs is also a critical stage in the BNPL implementation process. Ensure that all integration aspects, including payment processing, account management, and reporting, function correctly and meet your business requirements.

Step 8: Promote New Functionality

Once the BNPL integration is complete and tested, launch the feature on your B2B eCommerce platform. Promote the availability of BNPL options to your customers through marketing campaigns, email newsletters, and other promotional channels.

Step 9: Monitor and Improve

Keep an eye on how BNPL works for your business. Monitoring the performance of BNPL transactions after launch is crucial to identify any performance issues or technical glitches that may arise under real-world usage conditions.

Analyze data, listen to customer feedback, and stay up-to-date with market trends. Use this information to make adjustments and improve your BNPL strategy over time.

By following these steps, businesses can make BNPL work for them in B2B eCommerce, boosting sales, managing cash flow, and building better customer relationships.

Future trends

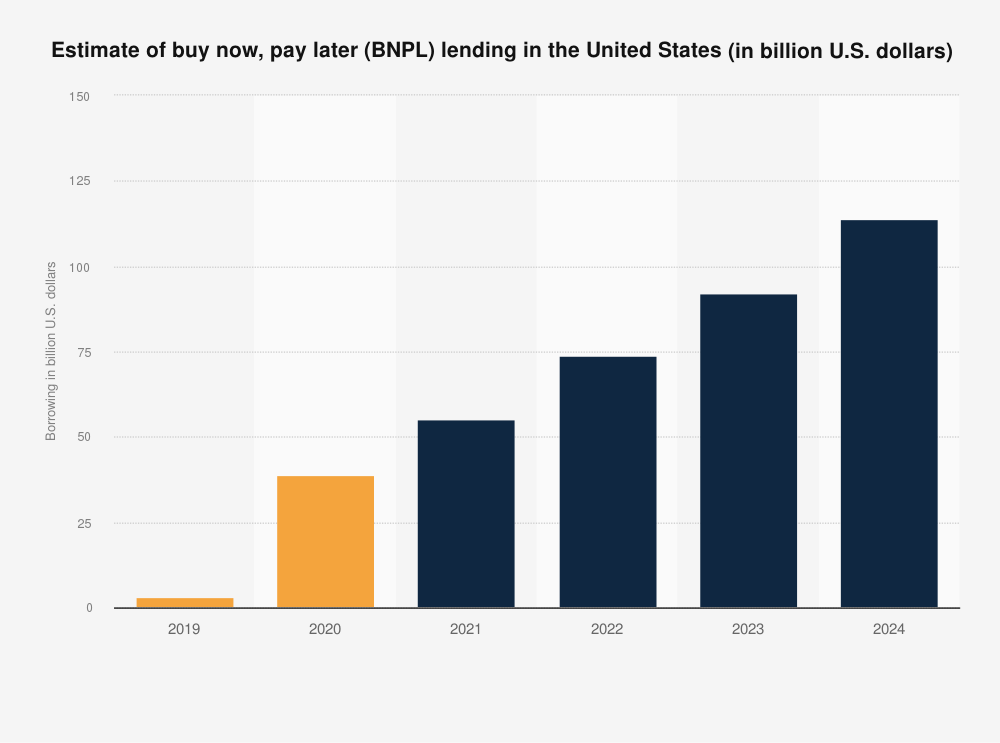

The U.S. BNPL Lending Market by Statista, 2022

Based on recent data, the popularity of BNPL B2B continues to rise steadily. In a notable statement from Justin Main, Vice President of Integrated Payments at Billtrust, a leading player in B2B accounts receivable automation and integrated payments, highlighted the potential benefits of BNPL for B2B transactions. Main emphasized the opportunity to reshape traditional credit card pricing models and reduce interchange costs, ultimately translating into cost savings for merchants, lower retail prices, and improved payment efficiencies.

Looking ahead, it’s crucial to recognize that BNPL is primarily geared towards small and medium-sized enterprises (SMEs). According to a study featured in Forbes, a staggering 99.9% of businesses in the USA fall into the SME category. As the SME sector continues to expand and existing businesses grow, the demand for B2B BNPL for small businesses is expected to follow suit, potentially reaching even greater levels of adoption in the future.

Conclusion

As B2B eCommerce continues to evolve, embracing BNPL represents not only a competitive advantage but also a catalyst for innovation and resilience in an increasingly dynamic business landscape. The integration of BNPL solutions presents a strategic opportunity for enterprises to enhance their purchasing processes and drive sustainable growth. By following a systematic approach to implementation, businesses can leverage BNPL to streamline transactions, improve cash flow management, and foster stronger relationships with their customers.

Ready to streamline your e-commerce operations? Elevate your business with seamless system integration for CS-Cart and Multi-Vendor platforms. Our experts are here to optimize your workflow, enhance efficiency, and boost profitability.